[금융위기 진단 1부] 미국 장단기 금리 역전 현상 발생

미국 2년-10년물 장단기 금리 역전현상이 발생하였다.

이것이 어떤 중요한 의미를 가지는지, 금융위기 진단에 어떤 지표가 되는지를 살펴보고자 한다.

Main yield curve inverts as 2-year yield tops 10-year rate, triggering recession warning

PUBLISHED TUE, AUG 13 2019 4:19 AM EDTUPDATED WED, AUG 14 2019 5:02 PM EDT

KEY POINTS

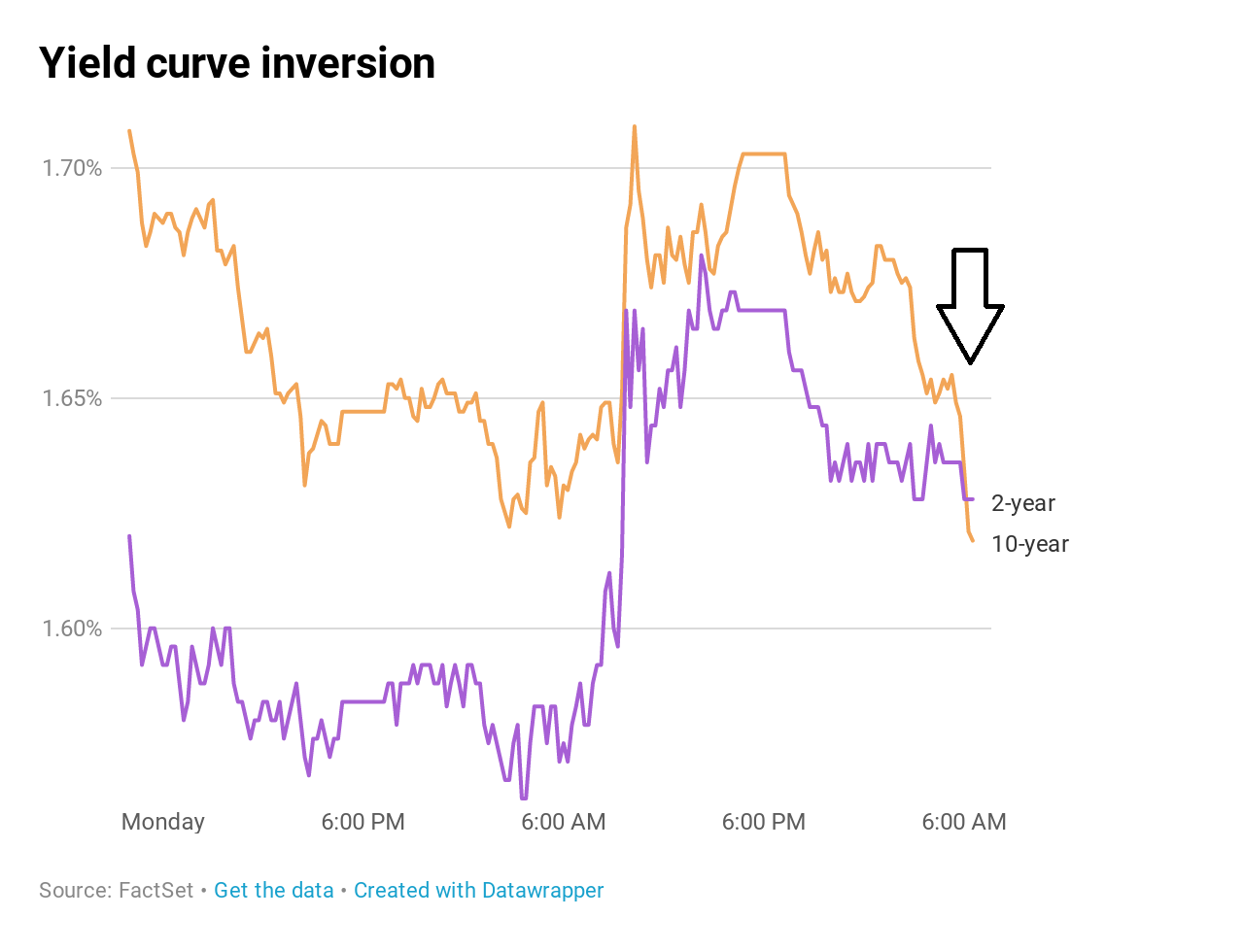

- Earlier Wednesday, the yield on the benchmark 10-year Treasury note was at 1.623%, below the 2-year yield at 1.634%. 수요일 오전 10년만기 국채수익률은 1.623%로, 2년만기 국채수익률 1.634%보다 아래로 떨어졌다.

- The last inversion of this part of the yield curve was in December 2005, two years before a recession brought on by the financial crisis hit. 국채금리 역전현상은 지난 2005년 12월이 마지막이었으며, 금융위기 발생 2년전 발생했다.

- A recession occurs, on average, 22 months following such an inversion, according to Credit Suisse. 크레딧스위스(스위스투자은행)에 따르면 국채금리역전현상 이후 평균 22개월 이후 경기불황이 발생한다.

The yield on the 30-year Treasury bond traded at 2.02%, well below its former record low of 2.0889% hit in 2016 following Britain’s Brexit vote. Yields fall as bond prices rise.

30년 국채수익률도 2.02%로 하락했으며, 이는 2016년 영국의 브렉시트 탈퇴 당시 최저수익률이었던 2.0889%를 경신한 수익률이다. 금리가 떨어지면 채권가격은 오른다.

The last inversion of this part of the yield curve was the one that began in December 2005, two years before the financial crisis and subsequent recession. Economists often give the spread between the 10-year and the 2-year special attention because inversions of that part of the curve have preceded every recession over the past 50 years.

지난 금리역전은 2008년 금융위기와 그 이후의 경제불황 2년 전인 2005년 12월 발생하였다. 경제학자들은 2년-10년 국채금리의 스프레드에 특별한 관심을 기울이는데, 지난 50년간 금리 역전현상은 경제 불황 전에 꼭 선행해왔기 때문이다.

Historical inversions of the 2-10 curve (recessions marked in gray)

Data from Credit Suisse going back to 1978 shows:

크레딧스위스 (스위스 투자은행) 의 데이터에 따르면 :

- The last five 2-10 inversions have eventually led to recessions. - 지난 다섯번의 2년-10년물 금리역전 현상은 최종적으로 경기불황으로 이어졌다.

- A recession occurs, on average, 22 months following a 2-10 inversion. - 2년-10년물 금리역전현상 이후 평균 22개월 후 경기불황이 발생하였다.

- The S&P 500 is up, on average, 12% one year after a 2-10 inversion. - 2년-10년물 금리역전 발생 1년 이후에 S&P 500 지수는 평균 12% 상승하였다.

- It’s not until about 18 months after an inversion when the stock market usually turns and posts negative returns.- 2년-10년물 금리역전현상 이후 18달 까지는 주식시장이 - 수익률을 보이진 않았다.

Going farther back in history, the yield curve’s track record gets a little more spotty. Post WWII, inversions have predicted seven of the last nine recessions, according to Sung Won Sohn, professor of economics at Loyola Marymount University and president of SS Economics.

역사적으로 살펴보면, 국채수익률 곡선은 조금 더 명확하게 보인다. 제2차 세계대전 이후, 금리역전 발생현상은 9번 중 7번의 경제불황을 예측했다. (손성원 교수)

“This is a track record any economist would be proud of,” said Sohn.

"2년-10년 국채 수익률 곡선을 추적하는 것은 경제학자들이 자랑스러워 할 일이다."

결과적으로, ① 장단기 국고채 금리역전현상은 경기불황의 징조가 맞다, 하지만 ② 경기불황은 이후 평균 22개월 뒤에 온다는 것을 확인하였다. 개인적으로는 경기불황까지 조금 더 대처할 수 있는 시간적 여유가 생긴 것이라고 생각한다.

그럼 이 상황에서 우리가 할 수 있는 것은 무엇일까??

우선적으로 생각해볼 수 있는 방안은 자산 현금화 & 달러 매수 두 가지일 것이다.

다른 지표들 또한 경기불황을 예측하고있는지 다른 시그널들을 차례로 알아보도록 하겠다.

'매요 insight 저장소' 카테고리의 다른 글

| 평범한 사람이 부자로 바뀌는 투자공식 (2) | 2022.02.03 |

|---|---|

| 원자재 ETF 모음 (구리, 원유, 귀금속, 농산품, 축산) (0) | 2021.10.04 |

| 산업통상자원부 수출입동향 (매월 1일 확인) (0) | 2021.08.22 |

| 원유ETF, ETN 종류, 그리고 롤오버/괴리율/콘탱고/백워데이션은 무엇인가?? (0) | 2020.04.09 |

| 코로나 경제위기 vs 과거 경제위기 비교 (0) | 2020.03.19 |